The Account Aggregator (AA) framework is rapidly emerging as one of the most impactful digital public infrastructure layers in India’s lending ecosystem. For lenders serving sole proprietors, small merchants, gig workers and micro-enterprises, cash-flow visibility is the foundation of risk assessment.

Bank statements and GST data remain the richest sources of truth — and how lenders access this data can dramatically influence underwriting speed, portfolio quality and operational efficiency. Across the business lending landscape, AA adoption is accelerating, but in varied ways. Here’s a consolidated view of how lenders are using AA today, and the strategic shift emerging across the credit lifecycle.

AA Adoption: What the Industry Data Shows

1. Mandatory AA Drives 70–100% Adoption

Lenders that embed AA as the primary data collection method consistently record the highest adoption. Clear journeys, strong digital flows and well-trained sales teams ensure predictable success rates and superior data quality.

2. Optional AA Leads to 20–60% Adoption

When borrowers or DSAs can choose between AA and PDFs, PDFs continue to dominate. Behavioural familiarity and operational convenience outweigh the benefits of real-time digital pulls unless the journey is redesigned to be AA-first.

3. Multi-Bank Data Is Becoming the Norm

Business borrowers typically maintain 2–3 active accounts for income, expenses and personal usage. Multi-bank AA consents are now essential for complete visibility and accurate cash-flow analysis.

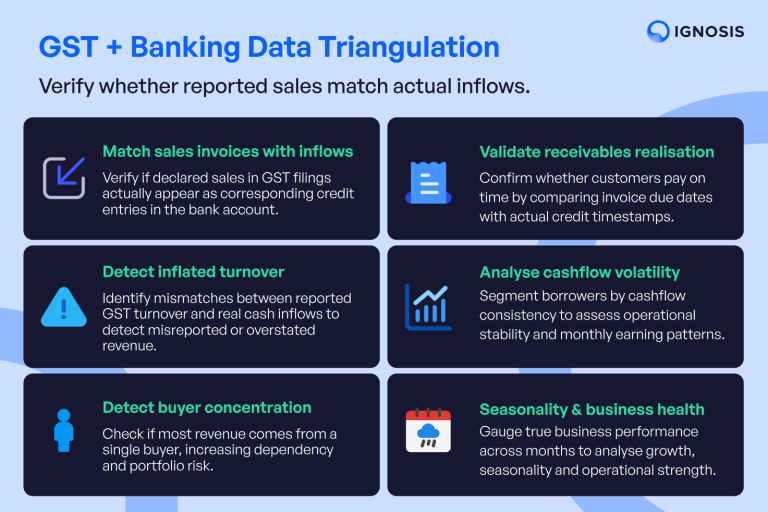

4. Insights Unlocked by Combining GST + Banking via AA

A fast-emerging trend is the triangulation of GST data (via AA) with banking cashflows to derive deeper underwriting intelligence.

With both data streams sourced digitally and consented through AA, lenders can now:

- Match sales invoices against actual credit inflows

- Validate whether receivables are being realised on time

- Detect inflated or misreported turnover

- Identify customer segments with delayed collections or high cashflow volatility

- Understand customer dependency on large buyers or single invoices

- Build a reliable proxy for business health and seasonality

This fusion of GST + banking data gives underwriters a real-time, accurate picture of business performance, far superior to PDFs or manually uploaded documents.

5. DSA & Sales Education Drives Real Adoption

AA adoption is not purely a product decision — it is a behavioural shift.

Lenders that invest in training DSAs and field teams see significantly higher adoption and smoother customer experiences.

A realistic view of current adoption patterns:

- 60–70% where strongly encouraged

- 20-40% where AA is optional

- PDF fallback remains necessary for certain borrower segments

AA Beyond Underwriting: The Next Unlock for Lenders

Forward-thinking lenders are now extending AA from underwriting to loan monitoring, early warnings and collections intelligence. This shift is unlocking powerful new capabilities.

1. Improved Collections Efficiency

Loan-monitoring consents allow lenders to:

- Track real-time inflows

- Time repayment nudges when liquidity enters accounts

- Reduce follow-ups and improve promise-to-pay conversions

2. Early Warning Signals (EWS) for Portfolio Health

Continuous, consented AA access enables lenders to detect:

- Drop in monthly credits

- FOIR deterioration

- New liabilities or EMIs

- Sector-level stress

- Irregular cashflow cycles

These allow proactive interventions before instalments slip.

3. Intelligent Top-Up Loan Opportunities

AA-powered monitoring highlights customers who become eligible for more credit:

- Improved FOIR

- Increased business inflows

- Reduced liabilities

- Seasonal growth opportunities

This enables contextual, pre-approved top-ups that enhance portfolio yield and customer retention.

Why Strong AA TSP Infrastructure Matters

As AA usage expands across channels, lenders increasingly depend on a robust TSP (Technical Service Provider) to ensure reliable, scalable, high-quality data access.

A strong TSP should offer:

- 100% FIP coverage, ensuring access to all major banks, cooperative banks and FI types

- Multi-FIP orchestration, enabling seamless retries, fallbacks and multi-account pulls

- Unified AA infrastructure across Direct, App, Web, Branch, DSA and Partner channels

- End-to-end support across underwriting, monitoring, collections and analytics

This ensures lenders don’t just adopt AA — they are able to scale it across their enterprise.

Conclusion

AA is becoming the backbone of cash-flow–based lending in India. Its real power, however, goes beyond underwriting — into continuous monitoring, collections intelligence, and personalised credit expansion.

Lenders that combine:

- AA-first journeys

- Multi-bank visibility

- GST + Banking triangulation

- DSA/sales enablement

- Lifecycle-wide AA monitoring

- A strong TSP with full FIP coverage

will build faster, safer and more profitable lending models.

AA is no longer just a digital rail — it is the intelligence layer that will define the future of credit.

.webp)

Powering India's next wave of financial data intelligence with AA-native infrastructure and enterprise-grade security.

.png)

.png)

© 2026 Ignosi Systems Pvt. Ltd. All rights reserved.