India has modernised credit rails. But recovery is still manual, manpower-heavy, and inefficient by design. This mismatch will define credit risk in the next 3 years.

India has built something extraordinary in credit. In a decade, lending has moved from branch-led paperwork to real-time, digitally underwritten, API-driven distribution. Digital lending volumes grew 251% between FY22 and FY25, with value jumping 208%. (Source: RBI Digital Lending Report)

We built a Ferrari engine for Lending, but kept the bicycle brakes for collections. While the front end of the credit lifecycle is fully digitised and frictionless, the backend hasn’t kept pace.

- We are underwriting and disbursing faster than ever

- But, recovery teams still operate without visibility into borrower liquidity or intent.

- Therefore, profitability of loans comes under pressure as volume scales

Collections costs rise almost linearly with headcount. For years, fintech differentiation came from distribution: faster onboarding, better funnels, embedded lending partnerships. The next long-term advantage lies in better collections.

We address it as an intelligence problem.

More people is not the answer

The efficiency gap persists not because lenders lack tools to reach borrowers, but because they lack the intelligence to know who to reach, when, and how.

Prioritisation of Efforts

In the last decade, AdTech evolved from spray-and-pray to hyper-targeted programmatic advertising. Marketers realised that showing the wrong ad to the wrong person was a wasted budget.

Channel allocation in collections feels stuck in the billboard era. Getting access to rich data sources (banking data, AA flows, Bureau history, central registries) is a solved problem. But most teams still lack the capacity to use them in real-time. Without this signal, distinguishing a self-heal customer who needs a nudge from a willful defaulter who needs intervention becomes hard.

Contactibility with borrower

The standard response to delinquency is aggressive follow-ups. That strategy has hit a wall due to the growing popularity of Caller ID apps and OS-level spam filtering. Aggressive dialing no longer guarantees contact; it actively degrades Right Party Contact (RPC) rates as algorithms flag high-volume numbers as spam.

Lenders aren’t just fighting borrower reluctance; they’re fighting the phone’s OS. Your most expensive resource, the human agent, spends their day battling spam filters instead of negotiating debt.

Probability of Mandate Execution Success

The costliest inefficiency lies in mandate execution: collecting based on the operational calendar (retrying a failed debit on T+3 or T+5) rather than borrower liquidity. Retrying against an empty account achieves nothing. It incurs bounce charges, inflates failure rates, and erodes goodwill.

Despite the maturity of the AA ecosystem, only a few lenders use daily EOD balance signals. If funds are there, trigger the debit. If not, wait.

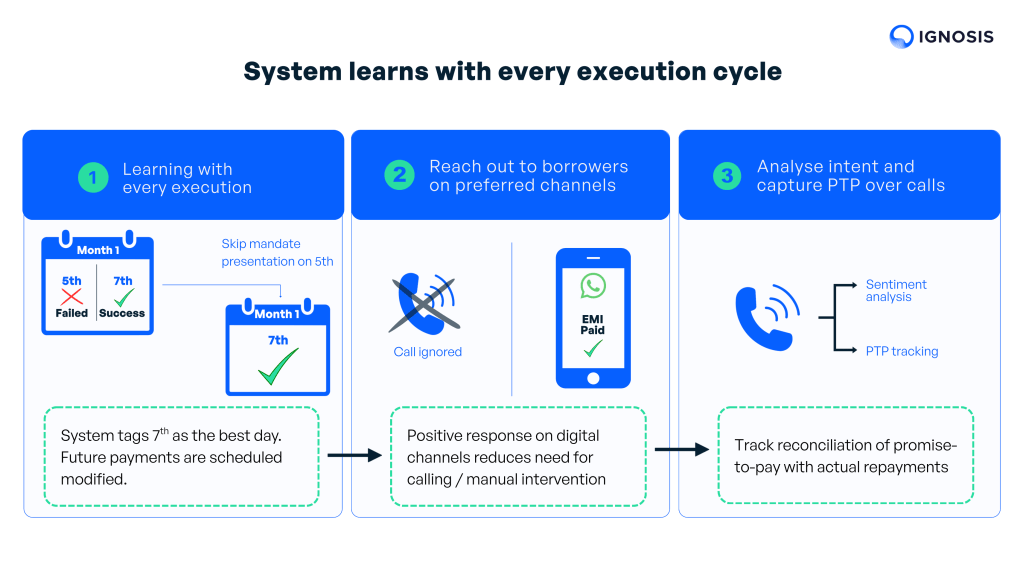

Outcomes improve when execution is combined with intelligence

Most lenders today run a siloed stack: the LMS holds the ledger, a separate dialer manages calls, a third-party gateway handles payments. The LMS knows a borrower is overdue, but the dialer doesn’t know why the last mandate failed.

The critical advantage of an end-to-end collections orchestration system is not speed; it is memory.

When one system owns the chain, performance starts improving with each collection cycle. Every recovery or bounce feeds back to sharpen case segmentation and allocation logic for the next cycle.

Financial data intelligence for collections

Imagine a scenario.

A borrower misses their EMI. Before triggering the standard escalation, the system checks: What’s their current account balance? Have they received their salary credit this month? Are there new EMI obligations that appeared after they took this loan? What’s their historical bounce pattern?

Interpreting their financial behaviour reveals why:

Scenario A: Temporary Oversight

Balance is healthy. Salary credited on time. No new obligations. Historical record shows no bounces. Likely a temporary oversight.

Action: Soft reminder via WhatsApp. Present mandate tomorrow when balance is at peak.

Scenario B: Temporary lack of funds

Balance near zero. No salary credit yet (usually comes by 7th, today is 12th). One new loan obligation visible.

Action: Wait. Flag for check on 15th. Don’t waste mandate presentation on certain failure.

Scenario C: Potential evasion

Large cash withdrawal three days before due date. Pattern matches previous defaults. Bureau shows new credit inquiries.

Action: Assign to agent. This needs human intervention, not automation.

This isn’t hypothetical. Financial data signals, processed correctly, can differentiate these scenarios in real-time.

3 pillars of modern collections

The modern recovery model has three pillars. Together, they form what India urgently needs to sustain its credit growth:

1. Intelligence-led segmentation

Not all delinquency is the same. Some customers are temporarily stressed. Some are chronically late. Some are willing but unable. Some are gaming the system.

Treating everyone with the same playbook is inefficient and counterproductive. Collections should be driven by behavioural segmentation and probability-led intervention.

2. Orchestration across rails

Collections is not just about communication. It is about execution. This includes mandate retries timed to cashflow cycles, dynamic payment links, UPI workflows, settlement intelligence, and channel switching based on response.

Manual workflows cannot orchestrate these at scale.

3. Consent-first data usage

This is where India is uniquely positioned.

Account Aggregator rails and consent-based finance create the possibility of collections that is both smarter and fairer – anchored not in coercion, but in insight.

When lenders can (with consent) understand cashflow patterns and capacity, they can prevent default earlier, reduce harsh interventions, offer better restructuring, and improve outcomes with dignity.

If you’re a bank or NBFC leader scaling credit:

- Reframe collections as strategic infrastructure, not operations.

- Build or adopt a collections OS that orchestrates channels, mandates, nudges, and interventions intelligently.

- Each process must become auditable – don’t rely on informal execution.

The end of the wild west

India’s credit expansion is one of the most important economic stories of this decade. But scale without stability is not progress.

The convergence of regulatory pressure and data privacy laws has turned improving collections into an existential necessity. FIDC’s recognition as a Self-Regulatory Organization (SRO) signals a definitive end to the Wild West era of recovery.

With the DPDP Act, scraping data or buying contact lists is now legally toxic. When borrowers consent to share financial data, collections become a transparent, defensible process. This makes Account Aggregator not just an operational tool but a compliance shield.

You can digitise lending in three clicks. But you cannot hire your way out of the recovery problem. To sustain 251% growth in digital lending, the back end of the credit lifecycle must finally get the same intelligence and horsepower as the front end.